Digital Bank

- Create your own neobank and offer financial services to your clients;

- Offer IBAN accounts to your clients;

- Get a Financial License EMI, MSB, SPI and carry out financial transfers for your clients.

- Payment transactions – transfers, acquiring, account management;

- Card issuance – virtual and physical cards for clients;

- Currency exchange – multi-currency accounts, P2P exchange;

- Lending – microloans, BNPL (Buy Now, Pay Later);

- Cryptocurrency transactions – purchase, sale, storage of cryptocurrencies;

- Investment services – purchase of shares, funds, bonds.

Digital Bank: The Complete Guide to Building Your Own Neobank.

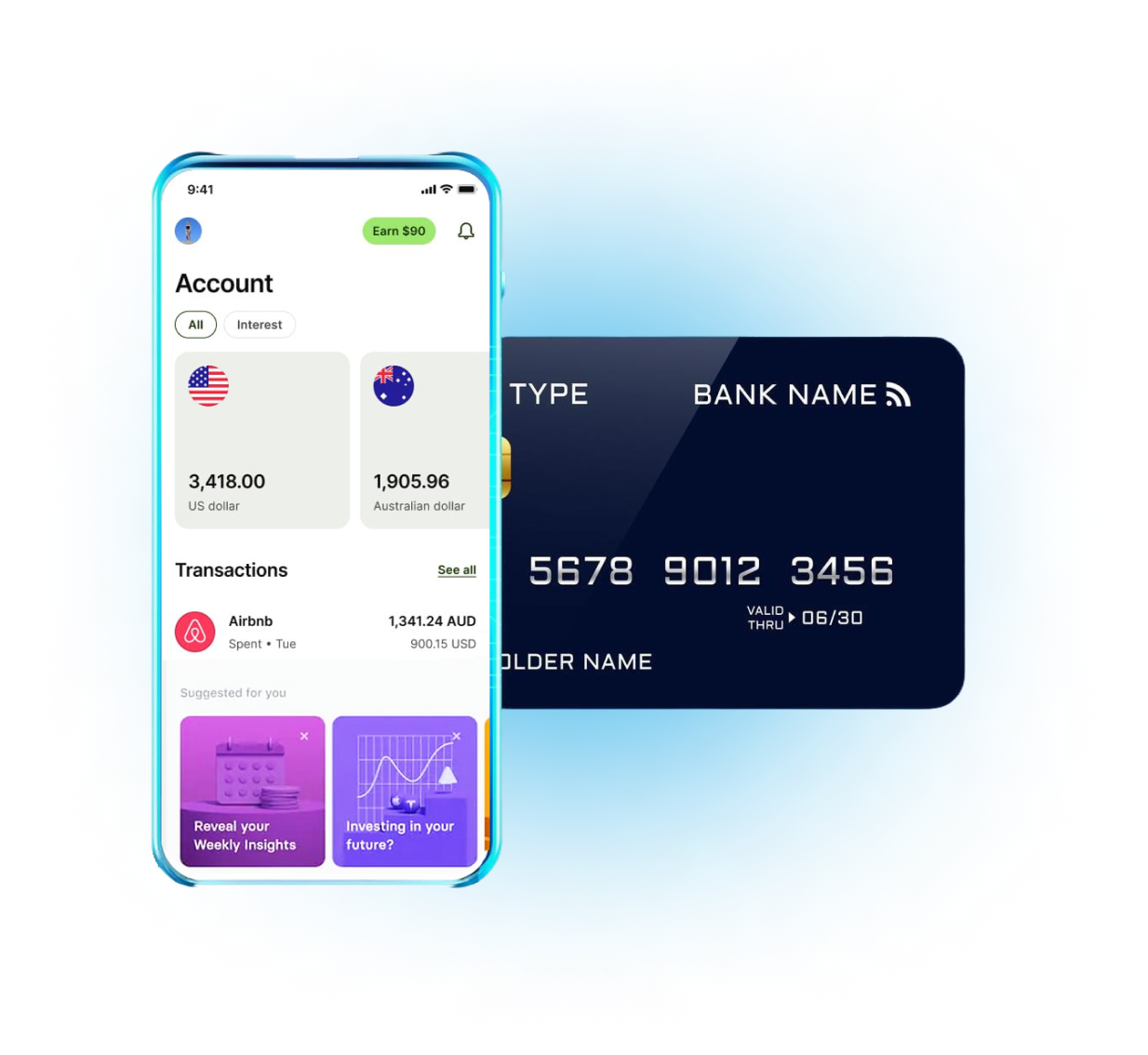

A digital bank (or neobank) is a financial institution that provides banking services without a physical branch. All transactions (transfers, payments, lending, currency exchange, investments) are carried out through mobile applications and web platforms.

Such banks operate on the basis of financial licenses and API technologies, which allows them to integrate with payment systems and provide convenient customer service.

Requirements for launching a digital bank

Company registration and obtaining a Financial License

Drawing up a company business plan, -Development of AML policy (Anti-Money Laundering), -privacy policy, -terms of use, -connection of KYC provider and ID Verification, -drawing up Risk, -Assessment Report (Risk assessment), -drawing up Operational Plan (Operational work plan), -connection to FINTRAC, WorldCheck, Equifax databases.

Connecting to a payment provider

Connecting a payment card provider, connecting acquiring processing, completing payment provider onboarding, replenishment, transfers, payments (SEPA, SWIFT, Faster Payments, etc.), issuing cards (virtual or physical), storing funds and processing transactions, describing the business model (what services are provided, how payments are processed), financial reporting, the provider analyzes how the business complies with their policies, checking the source of funding.

Development of fintech application

Key features of the application: User registration and authentication (2FA, biometrics), – Account management (balance, transaction history),

– Transfers and payments (P2P, accounts, international transfers), – Provision of IBAN accounts to clients,

– Virtual and physical cards (issue, freezing, limit management).

For EMI (Electronic Money Institution – electronic money license, EU):

- Authorized capital: from 350,000 euros;

- Company registration in the EU (Lithuania is one of the best jurisdictions);

- Availability of the KYC/AML system;

- Financial stability and audit.

For MSB (Money Service Business – financial services license, Canada, USA):

- Registration with FINTRAC (Canada) or FinCEN (USA);

- Compliance with AML/KYC requirements;

- Legalization of business and reporting to the regulator.

For SPI (Small Payment Institution – Small Payment License, EU):

- Authorized capital: from 20,000 euros;

- Limit on annual turnover (up to 3 million euros);

- Simplified audit requirements.

Regulation of digital banks

- Lithuania (EMI) – controlled by the Bank of Lithuania, part of the SEPA zone, operates under EU directives;

- Canada (MSB) – regulated by FINTRAC, registration and reporting required;

- Poland (SPI) – supervised by KNF (Polish Financial Supervision Authority), less stringent requirements.

- Selecting a business model – defining services (payments, loans, wallets, currency transactions);

- Choice of jurisdiction – registration of a company in a country with favorable conditions (Lithuania, Poland, Canada, etc.);

- Obtaining a license – choosing the appropriate license (EMI, MSB, SPI);

- Technical platform – development of a mobile application, integration with payment systems;

- Compliance with regulatory requirements – implementation of AML/KYC procedures.

With expert guidance from Lawskar, each stage — from business model design to regulatory compliance — is handled with precision and legal confidence, helping you launch a fully compliant fintech project faster and more efficiently.

Conclusion

Creating a digital bank is possible if you approach the process correctly. EMI, MSB and SPI licenses allow you to launch financial platforms, offering clients innovative payment solutions.

Want to launch your own neobank?

We will help you choose the best license and prepare your company for launch.

- Response within one business day

- Free initial consultation

already trust Lawskar

Arrange a Meeting

If you have any questions, suggestions or need advice, we are happy to help! Contact us in your preferred messenger:

Aleksei Shulyakovsky

Our professional team will find the best solution for your business!

Position

CEO, Founder LAWSKAR

lawskarglobal@gmail.com